5 Key Financial Metrics Every Small Business Owner Should Monitor and How to Interpret Them

In the dynamic world of small business, knowing your financial health is a superpower. It's more than just knowing what's in the bank; it's deep diving into the numbers that really matter to understand how your business is performing and its real potential. Keeping key financial metrics will change the game in how you run your business through insights that drive strategic decisions and fuel growth. This comprehensive guide proceeds to explain five critical financial metrics every small business owner should track, how to calculate them, interpret their significance, and the strategies for improvement.

1. Cash flow

Cash flow is the lifeblood of any business, showing an indication of how money moves in and out over time. It gives a view whether that business can meet obligations, take advantage of opportunities, or ride out financial storms.

Calculating cash flow:

- Cash flow = Cash inflows - Cash Outflows

Components of cash flow:

- Cash inflows: money coming in as a result of sales revenue, investments, loans, and any other sources of revenues.

- Cash outflows: include rental, salaries, utilities, and inventories bought.

Interpretation:

- Positive cash flow: Your business is generating more cash than it is spending. It's a vital element that survives in your business, and is needed to grow your business on a large scale and sustain it.

- Negative cash flow: This will indicate that your expenses are running ahead of your income, and if amortized in time, it may well lead to liquidity problems.

Pro tip:

Maintain a cash cushion sufficient at least to cover three- to six-months operating expense requirements. Sometimes this buffer is worth its weight in gold during periods of downturn or seasonal fluctuations.

Strategies for improvement:

- Optimize payment terms: By deciding on and negotiating better payment terms with suppliers you have the opportunity to extend your cash outflows.

- Improve collections: Automatic billing wherever possible and providing early payment discounts to customers can encourage quicker collections.

- Seasonal trends monitoring: This will study historical data on the prediction of cash flow in peak seasons.

2. Profit margin

If cash flow is the lifeblood, profit margin is the heartbeat of your business. It tells you how much of each dollar in sales translates into profit.

How to calculate profit margin:

- Gross profit margin=(Revenue−Cost of Goods Sold/Revenue)×100

- Net profit margin=(Net Income/Revenue)×100

Interpretation:

The greater this margin, the more efficient and effective is the pricing strategy.

Benchmark your margins against industry standards on a consistent basis, looking for opportunities to enhance or leverage competitive advantage.

Pro tip:

If the gross margin is quite healthy but the net margin is low, you have operational inefficiencies or overheads that are too high.

Strategies for improvement:

- Economy / Cost control : Regularly review expenditure and identify where cost reduction can be done without affecting quality.

- Pricing strategies: Some pricing adjustments should be made, or promotions should be offered to enhance sales without negatively impacting profitability.

- Operations: Reduce waste in operations by deploying process changes and technology upgrades to enhance productivity and yield cost savings.

3. Account receivable turnover

This is like a speedometer on your invoices, letting you know through what speed money is coming in from customers. In other words, this reflects how good your credit policies and processes of collection are.

How to calculate accounts receivable turnover:

- Accounts Receivable Turnover= Net Credit Sales / Average Accounts Receivable

Interpretation:

- The higher the ratio means collections are effective; the cash is coming in.

- Lower ratio may indicate problems in the credit policies or the customer's payment behavior.

Pro tip:

While going after the high turnover ratio, the balance has to be maintained so that not by aggressive collection practices the customer relationships get harmed.

Improvement strategies:

- Automated invoice: Automate the invoicing process using software, and set reminders for payment dues.

- Customer incentives: Allow early payment discounts or apply late payment penalties in order to incentivize timely collections.

- Credit policies review: Periodically review the creditworthiness of the customers before granting credit terms.

4. Debt-to-Equity Ratio

This is the ratio of debt to wholly owned funds that a firm uses to finance its operations. It is indicated as a measure of financial leverage and risk.

How to Calculate Debt-to-Equity Ratio:

- Debt to Equity Ratio = Total Liabilities / Shareholders Equity

Interpretation

- A high ratio implies a high dependence on debt. This might increase financial risk but could also increase equity returns if well managed.

- On the other hand, a low ratio reflects conservative financing, but it may also restrict investment opportunities.

Pro Tip:

It also varies depending on the industry; knowing what your norm is can help you determine how well your financial structure is holding up.

Improvement Strategies:

- Reinvest the profits: Look towards reinvesting, rather than taking on more debt, with the profits earned.

- Equity financing: Seek investors or partners that provide capital without adding debt.

- Cost control: Cut all the non-essential costs that can increase profitability and reduce dependence on debt finances.

5. Inventory Turnover

In the case of physical products, inventory turnover for physical product-oriented businesses measures how efficiently the inventory is being managed by comparing the cost of goods sold against average inventory levels.

How to Calculate Inventory Turnover:

- Inventory Turnover = Cost of Goods Sold / Average Inventory

Interpretation:

- High turnover suggests that the inventory is well managed, and the sales are high.

- A low level of stock turnover could indicate overstocking or poor sales, which implies the tying up of capital where it need not be tied.

Pro Tip:

Leverage data analytics to study the best-selling items and adjust the levels of inventory. This can be further augmented through just-in-time inventory systems.

Improvement Strategies:

- Data analysis: Perform periodic analysis of sales data to determine trends in product demand and perform necessary adjustments to inventory levels.

- Supplier relationship: It develops a relationship with suppliers. A good relationship with suppliers aids in developing flexibility in placing orders and hence reduces lead times within the business.

- Product line optimization: Position product range in sync with sales performance to purge slow-moving stock and promote fast-moving ones.

Broader Financial Indicators

Even though the above-mentioned five metrics are important, small business owners can take into consideration other metrics, the involvement of which will provide deeper insights into a company's financial health:

1. Return on Investment (ROI)

It helps to gauge the profitability of investments in marketing, equipment, or basically any area.

Calculation:ROI = (Net Profit / Cost of Investment) × 100

2. Customer Acquisition Cost (CAC)

It helps in evaluating the cost effectiveness of marketing efforts since it calculates how much it takes for a new customer to be brought in.

Calculation:CAC = Total Marketing Expenses / Number of New Customers Gained

3. Churn Rate

It is calculated as the percentage of customers who cease using a service or product within a specific time period.

Calculation:Churn Rate = (Customers Lost During Period / Total Customers at Beginning of Period) × 100

4. Working Capital Ratio

Represents the ability of a firm to meet its short-term liabilities using its short-term assets.

Calculation:Working Capital Ratio = Current Assets / Current Liabilities

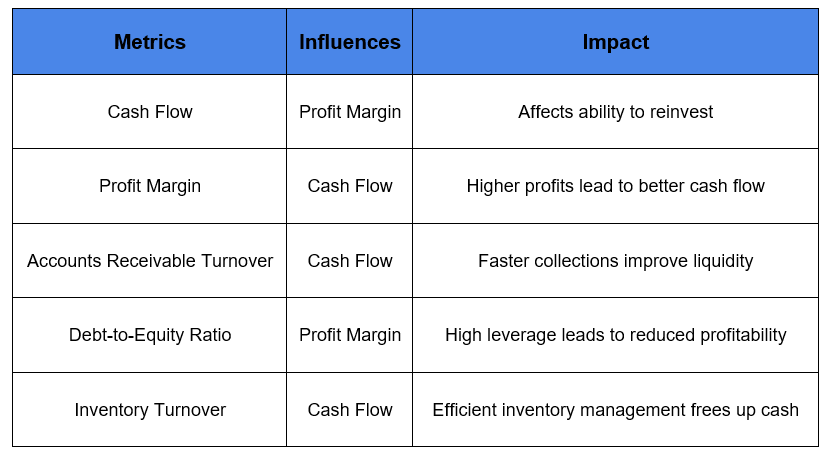

Interconnectedness of Measurements

Understanding how these metrics interact with one another is key in holistic financial management:

Technology and Tools

Incorporating technology into financial management can significantly enhance tracking and analysis capabilities such as:

Financial Management Software:

Examples of such metrics include QuickBooks, Xero, or FreshBooks, which are automatically tracked and reported for your convenience to help you save time and avoid mistakes.

AI-Powered Analytics:

AI-driven predictive insights from the historical hoc financial data recorded would let businesses prepare for future trends.

Solutions Dashboards:

Realizing dashboard solutions provides business owners with visualizations of key metrics in real time to easily identify trends and make quick, intelligent decisions.

Actionable Strategies for Improvement

What's more, for each metric discussed, small business owners should be able to go out and implement actionable strategies based on their own particular circumstances.

- To manage cash flow: Periodically review cash inflows and adjust the related payment schedules accordingly.

- For profit margins: Regularly review pricing in the prevailing market conditions and competitor analysis.

- For accounts receivable turnover: Establish clear payment terms with all customers in advance, and apply them consistently.

- For debt-to-equity ratios: Look to other methods of funding, which could include grants or crowdfunding, not increasing debt.

- Inventory turnover: Employ computer systems that monitor sales patterns in real time, thus enabling one to take proactive decisions regarding inventory.

Common Pitfalls

Owners of small businesses too often fall into the same traps in keeping abreast of their financial metrics.

- Ignoring seasonal variations: It leads to misjudging cash flow trends due to failure to account for seasonal changes

- Paying too much attention to a single metric: Many times, a single metric or ratio in isolation to the others can give the partial view about the financial health of an entity.

- Industry benchmark complacency: Not comparing metrics against industry standards could lead businesses astray with performance expectations.

Conclusion

Mastery of major financial indicators basically equips the small business owner with the knowledge to make informed decisions necessary for sustainable growth. These are, in fact, strong pointers to performance but need interpretation on relevant business models and industry dynamics. Being well-informed and proactive at the management of these metrics, positions your business to achieve not just survival, but its long-term success within an ever-evolving marketplace.

Make better decisions—without the guesswork.

Join 2,000+ pros getting real-time insights on finance, growth, and automation.

See What Your Business is Missing

Get instant answers, better decisions, and less guesswork—no setup stress, no tech skills needed.